In today’s fast-paced digital economy, the convenience of credit cards and UPI (Unified Payments Interface) transactions has revolutionized the way we handle money. A quick tap or scan, and you’re done—no more fumbling with cash or worrying about exact change. But beneath this convenience lies a silent crisis: poor money management and dwindling savings.

The Allure of Digital Transactions

Digital payment methods are designed to make spending effortless. Credit cards offer the allure of “buy now, pay later,” while UPI transactions provide instant payment solutions. However, this seamless experience often leads to impulsive spending, where you end up buying things you don’t need simply because it’s easy.

- Psychological Impact: When you swipe a card or make a UPI payment, it doesn’t feel like spending real money. This detachment from tangible cash often results in overspending.

- Small Purchases Add Up: Frequent low-value transactions, like ordering food or shopping online, can quietly drain your account over time.

Why Savings Are Taking a Hit

- Over-reliance on Credit: Credit cards encourage living beyond your means. High-interest rates and late payment penalties can spiral into a financial nightmare. Many people pay only the minimum due, which leads to accumulating debt.

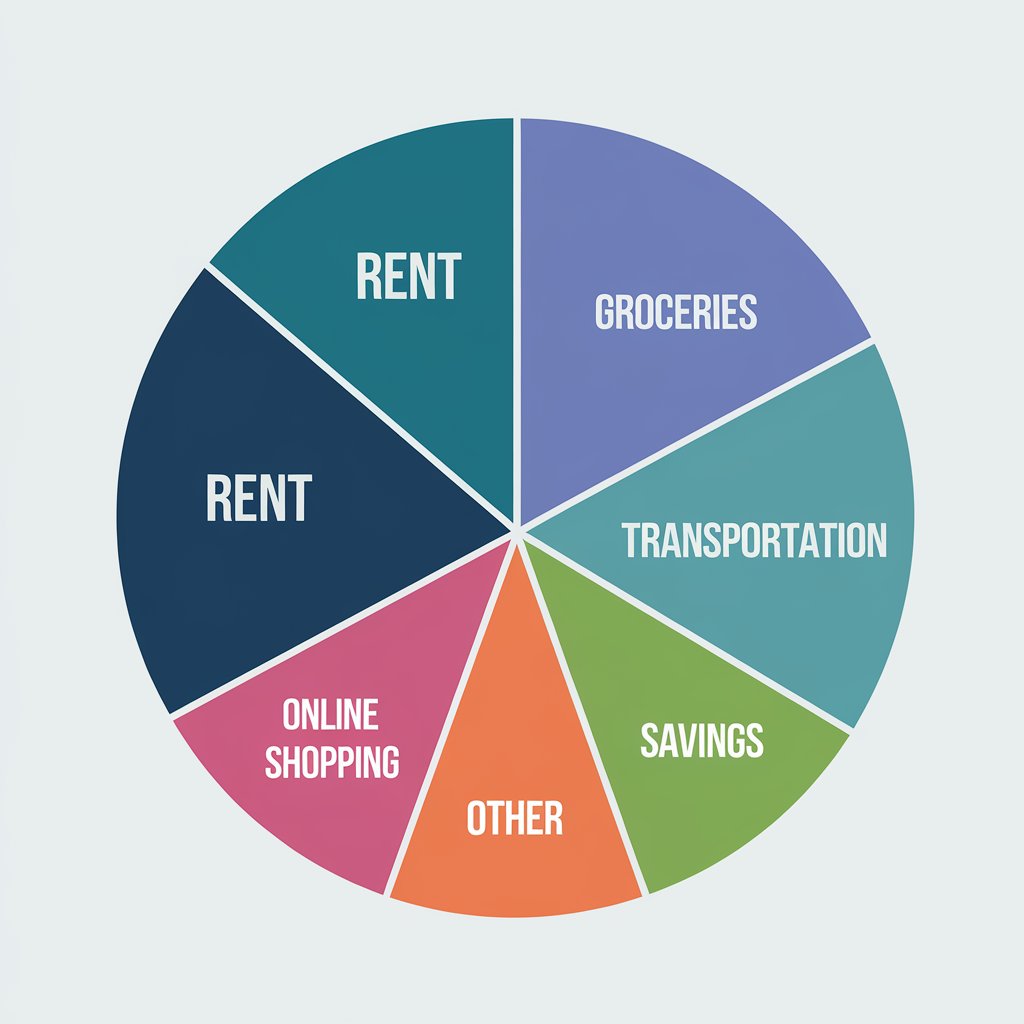

- Lack of Budgeting: With UPI making payments instantaneous, tracking expenses becomes challenging. Without a clear budget, it’s easy to lose control over where your money is going.

- Subscription Traps: Auto-debit features for subscriptions can silently eat away at your savings. You might forget about services you rarely use but still pay for every month.

- Social Pressure: The ease of digital payments also amplifies social spending. Whether it’s splitting bills with friends or indulging in online shopping sales, the “keep up with others” mentality can strain your finances.

How to Take Back Control

- Track Your Expenses: Use apps or spreadsheets to monitor every transaction. Categorize your spending to identify where you can cut back.

- Set Spending Limits: Most credit cards and UPI apps allow you to set daily or monthly limits. Use these features to curb impulsive purchases.

- Follow the 50/30/20 Rule: Allocate 50% of your income to essentials, 30% to discretionary spending, and 20% to savings. Make this a non-negotiable habit.

- Avoid Minimum Payments: Always pay your credit card bills in full to avoid high-interest charges.

- Build an Emergency Fund: Set aside at least 3-6 months’ worth of expenses in a separate account. Automate savings to ensure consistency.

- Pause Before Purchase: For non-essential items, follow the 24-hour rule. If you’re still convinced after a day, go ahead. Often, the urge to buy will pass.

The Path to Financial Discipline

While credit cards and UPI transactions are here to stay, financial discipline is the key to harnessing their benefits without falling into debt traps. By being mindful of your spending habits and prioritizing savings, you can regain control of your finances.

Final Thoughts

Money management in the digital age requires a conscious effort. The convenience of modern payment methods shouldn’t come at the cost of your financial well-being. Take proactive steps today to ensure that your future remains secure and stress-free.